Payment Processors Comparison 2026: Top Platforms, Features & How to Choose

A detailed comparison of the leading payment processors in 2026, covering APIs, PCI DSS compliance, local payment methods, settlement infrastructure, payouts, and global ecommerce scalability.

Compare the top payment processors in 2026 including Stripe, PayPal, Adyen, Square, Amazon Pay, and LimePay. Learn about APIs, payouts, PCI DSS, local payment methods, and global scaling.

Payment Processors Comparison 2026: Top Platforms, Features & How to Choose

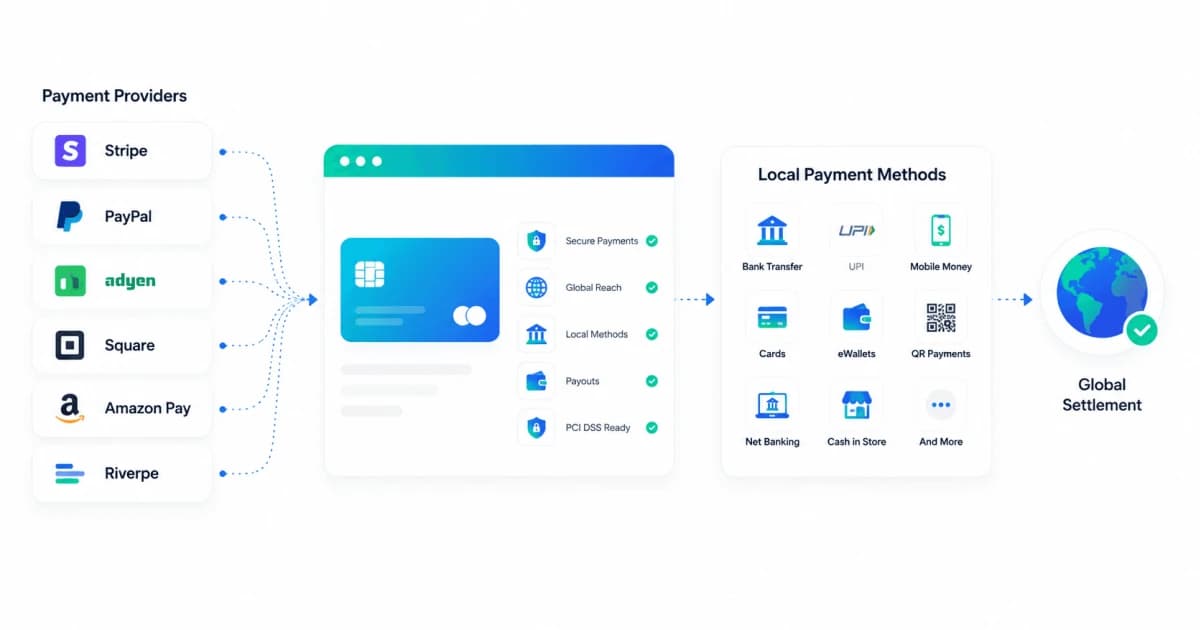

Digital payments in 2026 are no longer built around a single provider. For most online businesses, a payment processor functions as one layer within a much broader infrastructure that includes checkout orchestration, acquiring relationships, fraud prevention systems, compliance management, payout operations, and reconciliation workflows.

In practical terms, modern payment operations involve far more than simply accepting card payments. Businesses now need infrastructure capable of handling authorization flows, settlement logic, local payment methods, asynchronous payment events, dispute handling, and regional financial regulations — all while maintaining reliability at scale.

This payment processor comparison focuses less on marketing feature lists and more on the operational realities companies face once payment systems move into production. Instead of asking which provider is “most popular,” the more important question is how each platform behaves under real-world conditions:

- How reliable are the APIs during retries or timeouts?

- How well does the provider support webhook-driven payment states?

- Can the infrastructure scale across multiple countries and entities?

- Does the platform reduce PCI DSS exposure through tokenization?

- How effectively does it support local payment behavior in emerging markets?

- These factors often become far more important than simple integration speed.

The Most Popular Payment Processors in 2026

Several payment platforms dominate global ecommerce, but each is designed around a different operational philosophy. A provider that works well for a startup in North America may not be ideal for a platform expanding into Africa or Southeast Asia where local bank transfers and mobile money are essential for conversion.

One of the most common mistakes businesses make is selecting a processor solely because onboarding appears fast or developer documentation looks polished. As companies grow internationally, requirements around payouts, alternative payment methods, settlement reporting, and regulatory compliance become much more complex.

Below is a practical breakdown of the major payment platforms shaping ecommerce in 2026.

PayPal

PayPal remains one of the most recognizable payment brands globally and is commonly added as an additional checkout option because many consumers already trust and understand the experience.

Advantages

- Strong global brand recognition

- Familiar wallet-based checkout experience

- Broad international user adoption

- Straightforward implementation for many ecommerce businesses

- Publicly documented country and currency availability

For merchants operating in regions where PayPal adoption is already strong, offering PayPal can reduce checkout hesitation and improve customer confidence during payment.

Limitations

Despite its popularity, PayPal can introduce operational complexity in multi-provider payment environments. Settlement records, reporting structures, and transaction lifecycle behavior may not align neatly with other processors, making reconciliation more difficult for finance teams.

PayPal also has limitations in emerging markets where localized payment methods dominate consumer behavior. In many African and Asian markets, customers rely heavily on mobile money systems, domestic bank transfers, and regional payment rails that PayPal does not support as deeply as providers focused on local infrastructure.

Best Use Case

PayPal works best as a complementary payment method alongside cards and local rails rather than as the sole foundation of an international payment stack.

Stripe

Stripe is widely recognized for its developer-focused ecosystem and API-first approach. Many engineering teams choose Stripe because of its clean documentation, modern tooling, and relatively fast implementation process.

Advantages

- Developer-friendly APIs

- Strong documentation and SDK ecosystem

- Detailed guidance for international payment support

- Extensive support for subscriptions and recurring billing

- Broad ecommerce integrations

Stripe also publishes detailed documentation around payment method eligibility, country availability, and currency support, which helps businesses plan international rollouts more predictably.

Limitations

Stripe’s suitability depends heavily on the markets a business intends to serve. While the platform performs extremely well in many regions, support for localized payment rails varies significantly by country.

In markets where domestic transfers or mobile money systems dominate consumer payments, Stripe may require additional integrations or complementary providers to achieve optimal conversion rates.

Best Use Case

Stripe is particularly effective for SaaS companies, startups, and online businesses prioritizing developer velocity, subscription billing, and scalable APIs.

Adyen

Adyen is commonly associated with large-scale global commerce and enterprise payment operations. The platform is designed for businesses that need centralized governance, unified reporting, and consistency across multiple regions.

Advantages

- Enterprise-grade infrastructure

- Strong global acquiring network

- Centralized reporting capabilities

- Advanced tokenization support

- Suitable for complex international operations

Adyen’s architecture is often appealing to businesses operating across multiple markets because it emphasizes operational consistency and financial visibility at scale.

Limitations

Enterprise-focused systems typically require more implementation planning and operational discipline. Configuration management, testing environments, monitoring, and governance structures often become more demanding compared to lighter-weight platforms.

The trade-off is greater long-term control and scalability.

Best Use Case

Adyen is best suited for large ecommerce companies, marketplaces, and multinational businesses with complex global payment requirements.

Square

Square is particularly strong for businesses operating both online and in physical retail environments. Its ecosystem combines payment acceptance with operational tools such as inventory, point-of-sale systems, and business management software.

Advantages

- Strong omnichannel capabilities

- Integrated in-person and online payments

- Simple operational tooling

- Clear onboarding processes

- User-friendly ecosystem for smaller merchants

Square’s documentation clearly outlines country support and payment availability, which simplifies expansion planning for businesses operating within supported markets.

Limitations

Geographic coverage can become restrictive for companies expanding aggressively into international markets. Seller account availability and localized payment support are not as broad as some global-first platforms.

Best Use Case

Square is ideal for businesses with strong in-person commerce operations that also require online payment capabilities.

Amazon Pay

Amazon Pay leverages Amazon’s consumer ecosystem to simplify checkout experiences for users already familiar with Amazon accounts and stored payment credentials.

Advantages

- Familiar checkout experience

- Potentially faster conversions for Amazon users

- Multi-currency capabilities

- Reduced friction during checkout

Limitations

Amazon Pay is generally used as a supplemental wallet option rather than a complete payment processing solution. Businesses still typically require additional infrastructure for local payment methods, regional bank transfers, and broader global coverage.

Best Use Case

Amazon Pay works best for ecommerce merchants targeting consumers already engaged with the Amazon ecosystem.